Interest Rate Cuts: What They Mean for Vancouver Buyers and Investors

The Bank of Canada’s recent interest rate cuts have set the stage for a pivotal fall housing market in Vancouver. After two years of aggressive tightening, borrowing costs are finally easing, raising an important question:...

The Bank of Canada’s recent interest rate cuts have set the stage for a pivotal fall housing market in Vancouver. After two years of aggressive tightening, borrowing costs are finally easing, raising an important question: will this spark a resurgence in demand or simply provide a temporary breather for stretched buyers and investors?

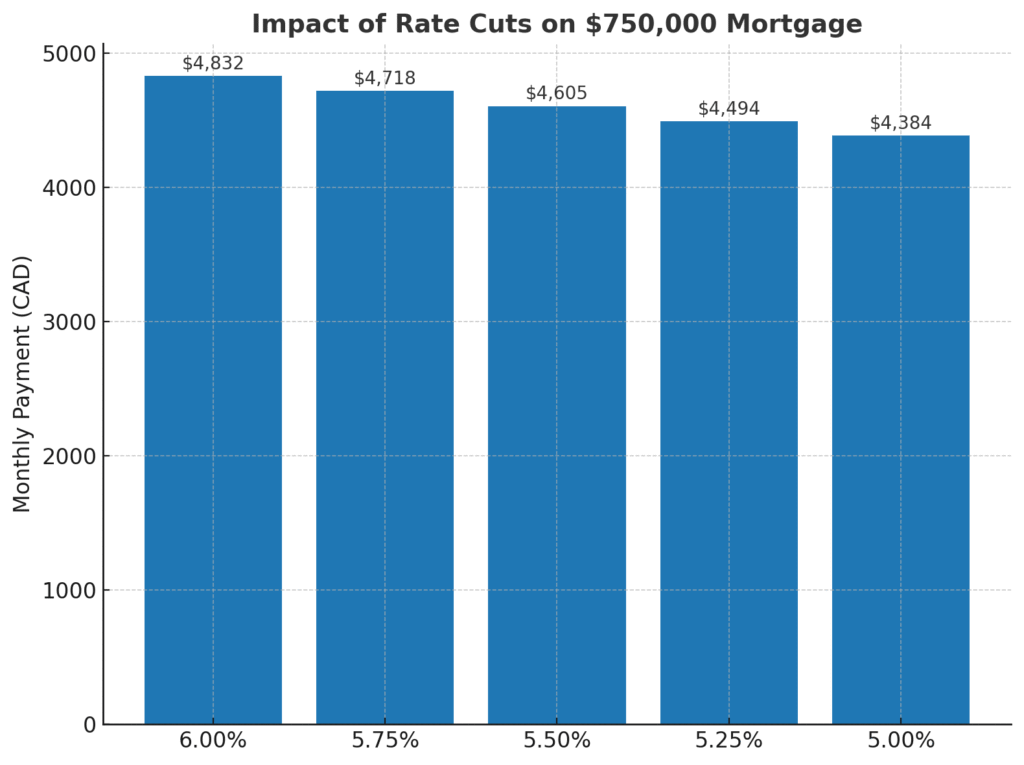

How Rate Cuts Affect Mortgage Payments

Every 25-basis-point cut may sound small, but it has a tangible impact on affordability. For example, on a $750,000 mortgage, a quarter-point reduction can save households around $120 per month. With multiple cuts expected through late 2025, buyers may see their monthly payments fall by several hundred dollars compared to earlier this year.

For variable-rate borrowers, the relief is immediate. Those with fixed rates will feel the benefit at renewal, where lenders are already offering five-year rates just below 5 percent for the first time in over a year.

Impact on Vancouver Homebuyers

Lower rates improve monthly affordability, but the bigger question is whether they will be enough to bring more buyers into the market. Vancouver’s average detached home price remains above $1.8 million, far outpacing income growth. Even with cheaper borrowing, stress test requirements still demand buyers qualify at rates roughly 2 percent above their contract rate.

This means entry-level buyers may feel some relief, but the affordability gap remains wide. First-time buyers are still leaning heavily on presale condos, where smaller deposit structures and longer completion timelines give them flexibility.

Impact on Investors

Investors stand to benefit differently. Lower rates reduce carrying costs on rental properties, improving cash flow in a market where rents remain strong. However, with active listings rising across Metro Vancouver, investors are weighing the risk of softer resale values against the long-term fundamentals of population growth and limited supply.

Some developers are also offering rate buydowns and assignment-friendly contracts on presales, which appeal directly to investors looking for flexibility.

Canada vs. U.S. Market Reaction

The U.S. Federal Reserve is also cutting rates, though American buyers enjoy the stability of 30-year mortgages. Canadian buyers, who must renew every few years, are more exposed to these shifts. This makes rate cuts a bigger short-term driver of sentiment in Canada than in the U.S.

Toronto is seeing a similar dynamic, with cautious optimism returning as borrowing costs ease. Calgary remains insulated, with demand driven more by affordability and migration than by rate fluctuations.

What This Means for Fall 2025

For Vancouver buyers, lower rates could create a window of opportunity this fall, particularly as listings remain elevated and sellers become more negotiable. For investors, the combination of lower carrying costs and presale incentives could make 2025 one of the most attractive years to enter the market in nearly a decade.

But the broader question remains: will easing rates reignite bidding wars or simply keep the market balanced? September’s data will provide the first real glimpse into how sentiment is shifting.